Source : EuropeanMarkets

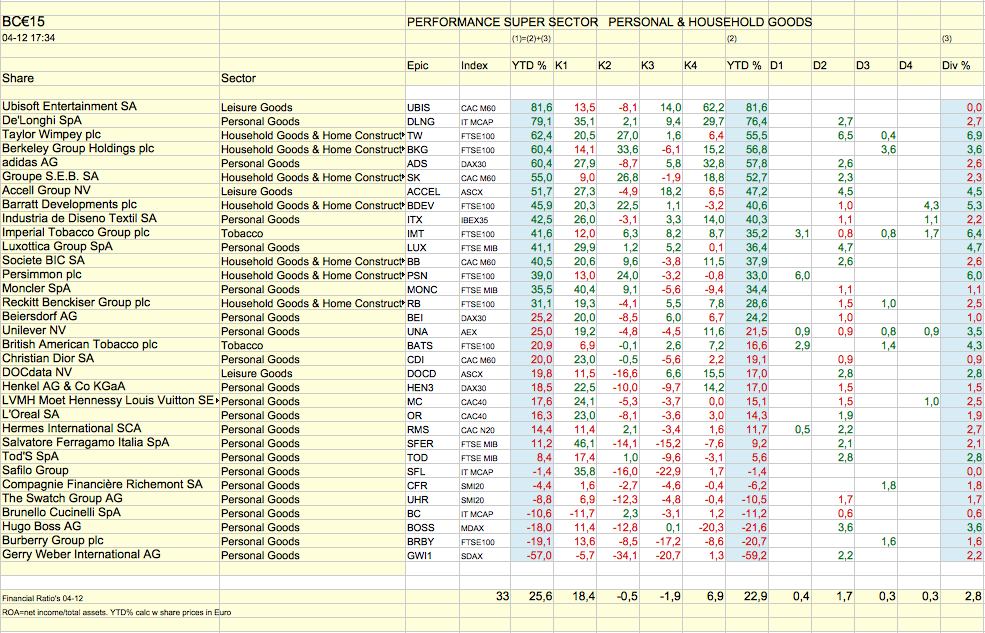

CEO Fabio de’ Longhi said “The performance achieved in 2015 witnesses the De’Longhi Group’s capacity to continue along its growth path, despite a highly competitive market and a materially adverse foreign exchange scenario. However, we do not expect that these unfavorable developments experienced throughout the year will be such to prevent the Group from achieving its targets on margins and cash generation, thanks to the commercial and organizational initiatives put in place by the Company”.

The De’Longhi Group’s 2015 consolidated revenues reached about € 1,891 million, up by about 9.5% (about +6.6% at constant exchange rates). During Q4 2015, the Group’s revenues totaled about € 676 million, approximately a +5.6% increase, or about +3.9% at constant exchange rates, compared to Q4 2014, which experienced a very sustained organic growth, partly linked to very favorable market conditions (such as very high sales in Russia, in anticipation of material price increases due to the Ruble’s devaluation).

Analyzing FY 2015 revenues by market, it is worth highlighting that all the Group’s geographical areas recorded a good growth, with the only exception of North East Europe, where revenues’ growth was more limited.

More in detail, Europe ended the 12 months with a +7.1% growth, led by South West Europe (up by about +9.8%, with strong performance in Italy, Austria, Iberia and Switzerland), while in the North East Europe area growth (up by some +2.9%) in markets such as Poland, Hungary, Czech Republic and Scandinavia was partially offset by an unfavorable performance in Russia and Ukraine, negatively affected also by a sharp devaluation of the local currencies.

The APA area (Asia-Pacific-Americas) revenues recorded a sustained growth, increasing by about +17.1%, also thanks to a positive foreign exchange contribution: among the markets that contributed the most to the overall performance we highlight North America, South Korea, Australia, China and Brazil.

The MEIA division (Middle East, India, Africa) ended FY 2015 with a revenues’ increase of about +10.1%, thanks to a particularly favorable foreign exchange impact: revenues at constant exchange rates suffered from the impact of the political and military crisis that affected part of the Middle-East area.

CEO Fabio de’ Longhi said “The performance achieved in 2015 witnesses the De’Longhi Group’s capacity to continue along its growth path, despite a highly competitive market and a materially adverse foreign exchange scenario. However, we do not expect that these unfavorable developments experienced throughout the year will be such to prevent the Group from achieving its targets on margins and cash generation, thanks to the commercial and organizational initiatives put in place by the Company”.

The De’Longhi Group’s 2015 consolidated revenues reached about € 1,891 million, up by about 9.5% (about +6.6% at constant exchange rates). During Q4 2015, the Group’s revenues totaled about € 676 million, approximately a +5.6% increase, or about +3.9% at constant exchange rates, compared to Q4 2014, which experienced a very sustained organic growth, partly linked to very favorable market conditions (such as very high sales in Russia, in anticipation of material price increases due to the Ruble’s devaluation).

Analyzing FY 2015 revenues by market, it is worth highlighting that all the Group’s geographical areas recorded a good growth, with the only exception of North East Europe, where revenues’ growth was more limited.

More in detail, Europe ended the 12 months with a +7.1% growth, led by South West Europe (up by about +9.8%, with strong performance in Italy, Austria, Iberia and Switzerland), while in the North East Europe area growth (up by some +2.9%) in markets such as Poland, Hungary, Czech Republic and Scandinavia was partially offset by an unfavorable performance in Russia and Ukraine, negatively affected also by a sharp devaluation of the local currencies.

The APA area (Asia-Pacific-Americas) revenues recorded a sustained growth, increasing by about +17.1%, also thanks to a positive foreign exchange contribution: among the markets that contributed the most to the overall performance we highlight North America, South Korea, Australia, China and Brazil.

The MEIA division (Middle East, India, Africa) ended FY 2015 with a revenues’ increase of about +10.1%, thanks to a particularly favorable foreign exchange impact: revenues at constant exchange rates suffered from the impact of the political and military crisis that affected part of the Middle-East area.

Source : Press Release De'Longhi, Treviso (Italy), January 25, 2016